In my last post, I covered Earthport, a public competitor in the cross border payments market. Now it is time for public competitor #2:

INTL FCStone

That is not a typo; that is the name of a public US company (INTL) engaged in cross border payments (among many other activities). Please don’t ask me how to pronounce the name; I was not even sure how to type it. (If these people are trying to remain unknown, they have a good start.)

INTL FCStone provides financial services to a predominately mid-market customer base. Services include:

- Commercial hedging (for companies with exposure to agricultural or other commodities markets)

- Market-making for “pink sheets” OTC stocks

- Clearing and execution for futures and options and,

- Global Payments

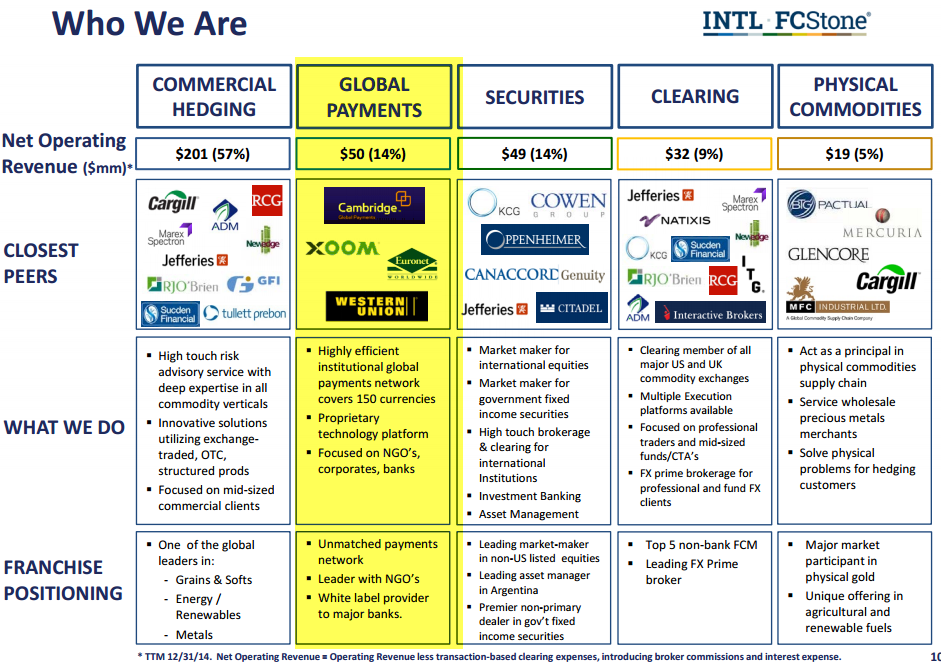

In an investor presentation, INTL FCStone describes itself as follows (my highlighting added):

Having learned that Earthport has attained an attractive market cap for a small, cross border payments business, I’m intrigued by that part of INTL FC Stone’s business.

INTL FCStone’s payments business is different from Earthport’s in a variety of ways:

- Intl FCStone’s started facilitating payments between granting organizations and NGOs in developing countries

- As a result, INTL’s commercial business does not seem as targeted at small payments, but more at supplier payments

- INTL’s business involves foreign currency exchange as much as processing; Earthport only recently added the currency exchange component

- INTL’s payments business is substantially larger than Earthport’s–more than 2x in revenue

- As you will see, INTL’s payments business is quite profitable, Earthport’s is not

Global Payments at INTL FCStone

It is hard to find clear non-financial information on INTL’s global payments offering. INTL seems to use the correspondent banking infrastructure but only at the local level, not in the middle. INTL FCStone has bank accounts in 150 countries and uses those accounts to transfer money. They clearly do their own foreign exchange transactions ,rather than relying on local banks with varying rates.

Fortunately, financial information on INTL FCStone’s payments business is readily available. The business is growing at about 15%+ annually and is very profitable. The growth rate is disappointing to me given the market growth rate, but I cannot argue with the profits. Here’s a chart of financial and underlying metrics from INTL FCStone’s investor deck:

Note the segment margin, which is before unallocated expenses from headquarters. (I checked allocatable expenses and even with those, the payments business is still quite attractive. The global payments business provides 14% of INTL’s revenue, but more than 20% of operating profits. Even more impressive, the cross border payments business uses about 2% of the company’s net assets, as is it not capital-intensive. (By contrast, the commercial hedging and market-making businesses are highly capital-intensive.) In short, buried in this company no one has ever heard of– is this nice, little gem.

INTL FCStone vs. Earthport Valuation

Earthport has a market cap of about $300 million or about 13x LTM revenue. Earthport’s payments business is growing nicely ($5-10 million per year), but is losing money and is half the size of INTL FCStone’s payments business. INTL FC Stone has a total market cap of $550 million, or $250 million more than Earthport. But for that extra $250 million you get a larger, more profitable cross-border payments business (growing at the same absolute dollar rate) plus a few other businesses generating $450 million in revenue. Some of these other businesses make money and a couple may not, but they do broaden the product line which can be sold to middle market customers. Here’s a summary of key valuation metrics for the two companies:

A few factors may be at play:

- Earthport’s payments business may be overpriced

- The value of INTL FCStone’s payments business may not be reflected in its stock price

- The two companies are in different ends of the global payments business and perhaps should not be compared so closely

- The rest of INTL FCStone’s businesses are not too valuable, as they capital-intensive and low-profit

I suspect all four factors above have some truth to them, but just in case #2 above predominates, I bought a little INTL FCStone stock for the fun of it!

{kind=link}

Recent Comments